- June 11, 2026

- Posted by: admin

- Category: BitCoin, Blockchain, Cryptocurrency, Investments

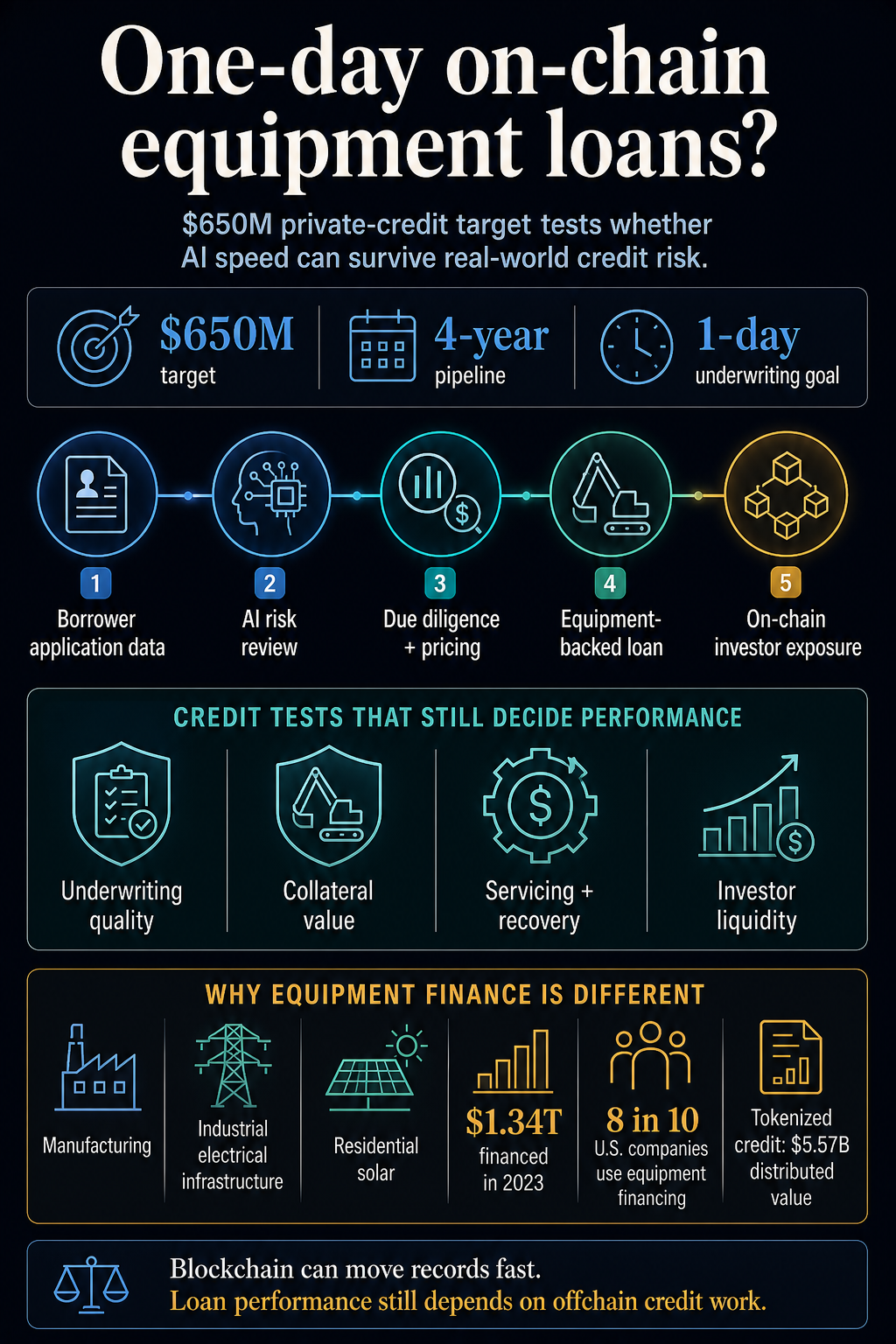

Equipment-financing lender Trad.Fi and autonomous-finance platform W3 are working on a plan to move a targeted $650 million private-credit origination pipeline onto blockchain rails over four years.

The plan targets U.S. equipment financing for sectors including manufacturing, industrial electrical infrastructure, and residential solar, with AI assessing risk, conducting due diligence, and pricing loans quickly enough to compress a process that can take months into a single day for small and mid-sized businesses.

That makes the project a clearer real-world asset test than another tokenized fund wrapper. Tokenization can record ownership and move investor interests across programmable rails. Repayment, collateral value, lien enforceability, and investor exits still depend on credit work outside the token itself.

Trad.Fi presents itself as a platform connecting borrowers and lenders to make equipment finance faster and more accessible. W3 describes its product as an operating system for autonomous finance, built to bridge legacy systems to digital rails and give enterprises control over agent-powered financial workflows.

The overlap is clear: equipment finance has paperwork, fragmented data, manual review, and private capital pools. W3 is pitching automation and auditability for financial workflows. Speed can change the borrower experience, while the credit product remains exposed to underwriting, collateral, servicing, and liquidity tests.

Underwriting remains the bottleneck

Trad.Fi’s borrower-facing materials say the platform sources capital from private institutions, analyzes borrower data in minutes, extracts information from equipment purchase orders, and sends applications for review by partner credit institutions in the United States.

Its lending page says accredited investors can access private lending pools that finance equipment-backed loans, with risk assessment using proprietary algorithms and external assessment from U.S. credit reporting agencies and financial institutions.

The borrower and lender pages put the real test on the credit file. The project turns on whether a lender can automate enough underwriting work to make equipment financing move at software speed while preserving the judgment that keeps private credit from becoming mispriced debt.

Equipment finance differs from tokenized Treasuries or tokenized public stocks. A Treasury fund depends on custody, compliance, transfer rules, and redemption mechanics around highly standardized assets.

An equipment loan depends on borrower cash flow, the value and resale market for the equipment, lien documentation, insurance, servicing, repossession, and recovery if the borrower stops paying.

The U.S. equipment-finance market is large enough for the experiment to matter. The Equipment Leasing and Finance Association says $1.34 trillion of U.S. equipment and software investment was financed in 2023, and more than 8 in 10 U.S. companies use some form of financing when acquiring equipment.

Against that market, a $650 million four-year target is modest. It is still large enough to test whether tokenized private credit can move out of portfolio wrappers and into operating-company lending.

The reported structure also carries an important caveat. The initial phase is expected to rely on institutional capital from traditional private-credit lenders to fund most underlying equipment loans directly offchain, while the companies work on bridge technology and a tokenized liquidity pool for eligible investors’ exposure to equity portions of the credit generated by the program.

That means the early test may be hybrid: real loans, offchain capital, and on-chain investor exposure, rather than a fully native blockchain credit market from day one.

| Claim | Credit test |

|---|---|

| AI compresses equipment-finance review into one day | Delinquency, loss, and recovery data must show speed preserved underwriting quality |

| Blockchain rails improve capital workflows | Investors need clear records, transparent cash flows, enforceable rights, and token balances that match legal claims |

| Equipment-backed loans create real-world collateral | Collateral values, liens, insurance, servicing, and repossession have to survive borrower stress |

| Tokenized exposure improves access to private credit | Liquidity terms, eligibility rules, and secondary-market depth must be disclosed and tested |

Private credit needs more than fast rails

Crypto’s RWA story has already moved past whether traditional assets can be represented on-chain. The unresolved test is whether those assets become useful inside open financial markets, or remain permissioned records with limited liquidity.

CryptoSlate previously reported that the tokenized RWA market was near $30 billion while only $2.47 billion was active in DeFi. The same analysis found private credit was more DeFi-active than Treasuries, commodities, or equities, partly because lending instruments are closer to DeFi’s native use cases than tokenized ownership products built mainly for regulated holding.

That context helps explain why equipment finance is a stronger RWA test than a new Treasury wrapper. Private credit already has an income stream, a borrower, and a repayment schedule. It can look like something DeFi understands.

It also carries the parts that remain difficult for DeFi at scale: cash-flow risk, legal recovery, servicing, and collateral enforcement.

A separate CryptoSlate analysis of Aave and corporate credit found that U.S. commercial and industrial lending reached $2.89 trillion at commercial banks, while on-chain lending markets still mostly price liquid collateral risk.

Aave can calculate loan-to-value ratios, liquidate collateral, and price stablecoin liquidity in real time. A lender financing machinery or solar equipment has to underwrite businesses whose repayment depends on operations, margins, invoices, and the resale value of physical assets.

That is where Trad.Fi and W3’s AI pitch becomes consequential. If AI can process purchase orders, borrower data, third-party credit inputs, equipment information, and lender rules faster than a manual process, the borrower gets capital sooner and the lender can move more files through the same operating base.

If the model misses weak borrowers, inflated equipment values, or deteriorating sector conditions, the same speed becomes a faster path to credit losses.

Loan seasoning will matter more than the size of the origination target. Delinquency, loss, and recovery data will decide whether the one-day workflow improves private credit or simply accelerates its weak points.

The investor test is liquidity and loss data

Tokenized credit dashboards have moved private credit beyond theory. RWA.xyz shows tokenized real-world assets in the low-$30 billion distributed-value range and tokenized credit at $5.57 billion in distributed value, though its live dashboards move enough that exact figures should be refreshed before publication.

CryptoSlate’s aggregate market page showed a $2.11 trillion crypto market, $82.4 billion in 24-hour volume, and 58.1% Bitcoin dominance at retrieval, but broad crypto pricing is only backdrop here.

The relevant metrics are how much of the credit exposure is actually on-chain, how investors receive cash-flow information, how transfer restrictions work, whether eligible investors can sell or redeem, and how defaults are handled.

A tokenized liquidity pool can make private credit easier to subscribe to. The asset class still has structural liquidity limits, and tokenization does not erase the need for clear terms, performance data, and default procedures.

A planned programmable treasury could eventually route senior and equity capital through Avalanche. For now, the near-term risk remains borrower repayment, collateral protection, and investor terms.

A borrower still has to repay. Collateral still has to be protected. Investors still need to know whether they own a liquid interest, a gated fund position, or a digital record of exposure to loans funded elsewhere.

However, the real answer may be conditional. AI-underwritten on-chain private credit is a credible blockchain-finance use case if automation produces better credit files, faster approvals, cleaner investor records, and transparent performance data without weakening risk controls.

It is a faster wrapper around offchain lending risk if the blockchain layer records exposure while underwriting quality, collateral control, servicing, and recoveries remain opaque.

The next signal is disclosure on the tokenized pool operator, on-chain loan lifecycle, AI governance, and first-cohort loan performance. Until then, the promise is clear: one-day equipment loans on blockchain rails. The test is whether those loans still look sound after time and stress do their work.

The post Lenders want AI to turn months of private-credit paperwork into one-day on-chain loans appeared first on CryptoSlate.